When the bridge becomes a chokepoint: what the Manus block tells Singapore companies about being “neutral”

Pulse Tan

8 min read

When Beijing blocked Meta’s US$2 billion acquisition of Manus on Monday, the immediate reading in the press was that this was about US-China tech decoupling, the limits of “Singapore-washing”, or Mark Zuckerberg’s AI strategy hitting a Beijing wall.

All of that is true. But sitting in Singapore, watching this play out, I think the more interesting question is the one closer to home: what does this episode actually mean for the country trying to position itself as a neutral AI hub, and for the Singapore companies operating under that flag?

What happened, briefly

The bare timeline: origin → transit → US$2B Meta deal → Beijing block, 27 April 2026.

Manus was founded in China by the team behind Butterfly Effect, made global noise in early 2025 with one of the first credible “general agent” products, and by mid-2025 had relocated its headquarters and most operations to Singapore. In December 2025, Meta announced a roughly US$2 billion acquisition. Meta would absorb the team and technology; Manus would shut its remaining China operations.

In January, Beijing opened a national security and export-control review. The two co-founders were barred from leaving China. On 27 April 2026, China’s National Development and Reform Commission ordered the deal unwound. Meta has signalled it will likely comply. Whether the unwinding can actually be completed is unclear, since the company, the team, and presumably the IP have already been substantially absorbed into Meta.

That is the bare timeline. The interesting parts are the implications.

The “neutral hub” story has always been two stories

Singapore has, for the last few years, been described in international press as a “neutral AI hub” or a “bridge” between the US and China. It is a flattering framing, and it has been useful. But it has been doing two very different jobs at once.

Singapore-Washing vs Singapore-Grown — regulators in Washington and Beijing can no longer distinguish these two at first glance.

One job is hosting Singapore-grown AI companies, and Singapore-grown AI capability inside SMEs and larger firms, in a jurisdiction that international clients trust. This is the part that benefits us directly. It is the version of the story where Singapore engineering, Singapore data governance, and Singapore corporate structure produce products that are credibly not subject to capture by either Washington or Beijing.

The other job is providing a redomicile address for companies whose technology, talent, and origin remain Chinese, but who want to present a different face to Western customers and investors. This is the “Singapore-washing” version, and it is the one the Manus block has now publicly broken.

These two stories have always coexisted. The trouble is that to outside observers, especially regulators in Washington and Beijing, they look identical at first glance. The Manus episode just made that ambiguity expensive.

What Beijing actually said, and why it matters

The official Chinese position, articulated through the Ministry of Commerce and the NDRC over recent months, is more precise than the headlines suggest. Beijing is not trying to stop Chinese firms from operating internationally. ByteDance, with TikTok, remains the standing example of what is acceptable: international expansion that keeps the core technology, data, and engineering ecosystem rooted in China.

Corporate identity at face value is no longer accepted. Technological nationality follows where the technology was built.

What Beijing is moving against is redomicile as exit. The Manus case establishes the doctrine that technological nationality follows where the technology was built, not where the company is registered. If your founders are Chinese citizens, your model was trained in China, your engineers were trained in China, and your IP originated there, then a Singapore corporate address does not change what you fundamentally are from Beijing’s perspective. It is a position that Lizzi Lee at the Asia Society Policy Institute and Le Xu at NUS Business School have articulated more sharply: corporate identity at face value is no longer accepted by either superpower.

Washington has reached a similar conclusion from the other direction. US regulators are increasingly looking at the full vertical of ownership, supply chain, data flows, and operational control rather than the legal headquarters. The Shein scrutiny is the cleanest example.

Both capitals now look at the full vertical — ownership, supply chain, data flows, operational control — not the legal headquarters.Corporate shell provides 0% mitigation if foundational layers remain in contested jurisdictions.

Both capitals have, in effect, converged on the same audit standard. Singapore-as-flag is no longer enough on its own.

The awkward truth about “neutrality”

The Singapore government does not actually claim neutrality. The pitch is principled non-alignment.

The Singapore position, articulated repeatedly in recent dialogues with industry, is that we do not actually claim neutrality. The argument is that being neutral results in being pulled into a tug of war by major powers. Singapore instead operates on a set of principles, fundamentals, and non-negotiables, communicated candidly to all parties, with positions taken on the basis of national interest. That is a different posture from neutrality. It is closer to what diplomats call principled non-alignment.

The distinction matters for Singapore companies. If you read the international coverage, you would think the country’s pitch is “we are Switzerland for AI”. If you read what the government actually says, the pitch is “we are a reliable jurisdiction with predictable rules and a clear sense of our own interests”. These are not the same product, and they attract different customers.

The Manus block heavily penalises companies relying on the Marketed Myth framework.

The first attracts companies looking for a place to hide. The second attracts companies looking for a place to build. The Manus block has just made it costly to confuse the two.

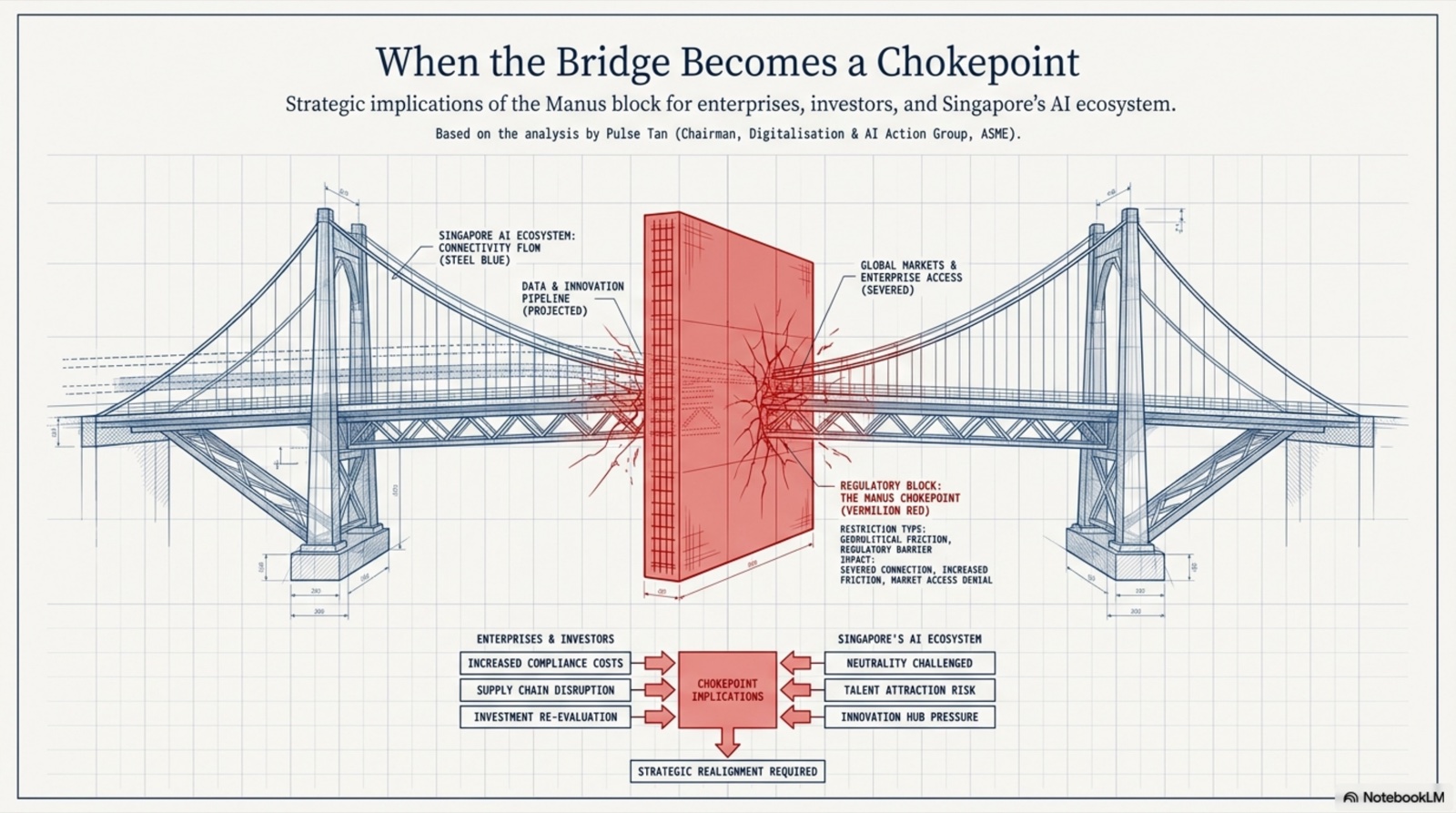

What this means for genuine Singapore companies

The four downstream effects we now have to price in.

First, the “Singapore address” premium is going to compress for ambiguous companies, and possibly expand for unambiguous ones. Genuinely Singaporean AI companies, with Singaporean or naturalised founders, Singapore-trained or Singapore-employed engineers, Singapore-resident data, and operations that are not a thin layer over Chinese infrastructure, are about to look more credible by contrast. Investors and enterprise customers who previously gave a small premium to any Singapore-registered AI firm are now going to ask harder questions. The firms that can answer those questions cleanly will benefit.

The generic "Singapore Address Premium" is dead. Genuine local firms face less competition for the trust they earn.How investors and customers will now distinguish the two — and price the difference.

Second, SMEs adopting AI need to start reading the geopolitical fine print of their tools. This is the practical part. If your accounting team is using a tool that was Chinese-founded but Singapore-headquartered, your data may sit in a place that is one regulatory action away from sudden change of ownership, sudden withdrawal, or sudden escalation. The Manus episode is not just a story about big M&A. It is a preview of the kind of whiplash that downstream users now have to price in. The two-month rule of thumb I suggest to SMEs I work with: ask where the IP is incorporated, where the founders are passport-holders, where the engineering team physically sits, and where customer data is stored. If those four answers do not point to consistent jurisdictions, you are accepting more political risk than your procurement officer has probably told you about.

The two-month rule: if these four inputs do not point to consistent jurisdictions, you hold unpriced political risk.If a vendor is Chinese-founded but Singapore-headquartered, your data sits one regulatory action from sudden escalation.

Third, the talent corridor is going to get more contested, not less. The MiroMind episode, where Beijing told the company not to send talent abroad after it expanded to Singapore, Japan, and the US, suggests that Chinese AI engineers will increasingly face friction in moving to Singapore even on legitimate paths. This is bad for Singapore’s AI capability building if we relied on that flow. It is, separately, an argument for taking ITE, the polytechnics, the universities, and the SkillsFuture pipeline more seriously as the substrate for AI capability rather than as a fallback. We cannot assume the imported-talent tap stays open at the rate it has been.

Beijing has signalled it will limit talent outflows. Singapore can no longer rely on the imported-talent tap.

Fourth, the brand cost is real. The phrase “Singapore-washing” has now entered the international vocabulary, and unfortunately it does not draw a clear line between cynical redomicile and legitimate relocation. NUS’s Chong Ja Ian has flagged the risk that Singapore is seen as a grey space for technology transfers, which one or both major governments may eventually move to restrict. That is the strategic exposure we should not pretend away. Every Manus-style story costs the legitimate Singapore AI ecosystem a bit of credibility it did not earn the discount on.

"Singapore-washing" is now an entrenched international term — and the legitimate ecosystem pays the rent.

What I am watching next

A few things would change my read of this materially. If Beijing accepts a partial unwinding that allows Meta to keep some of the technology and personnel, the deterrent effect of the block weakens, and the redomicile route stays half-open. If Beijing pushes for full reversal and gets it, the door is effectively closed and we should expect a wave of Chinese AI founders making earlier and harder choices, some of which will land in Singapore as genuine relocations rather than transits. Neither of those outcomes is bad for Singapore in the long run, as long as the country is honest about which kind of company it is hosting.

Neither outcome is bad for Singapore long-term, provided we stay honest about what we are hosting.

The bigger question is whether Singapore’s official posture stays principle-based or drifts toward a marketed “neutrality” that we cannot actually deliver. The first is durable. The second is rented credibility, and the rent has just gone up.

The bottom line

The Manus block is being read in three capitals as a story about US-China decoupling. From Singapore, I think it is more useful to read it as a stress test of our positioning. The “neutral hub” branding has worked when the stakes were low. The stakes are no longer low. What we have to defend now is not a flag of convenience for transit firms, but the underlying claim that Singapore-grown AI is a substantive category, with substantive standards behind it.

For Singapore SMEs and Singapore-grown AI companies, this is, on balance, an opportunity. The bar for what counts as credibly Singaporean has just risen, and the firms that can clear it have less competition for the trust they earn.

For everyone else, including those of us in policy circles who have been comfortable with the looser version of the story, the Manus episode is the cue to tighten up the language and start telling the truth about what we are actually offering.

The Manus block is not a technology story. It is an audit story.

When Beijing blocked Meta’s US$2 billion acquisition of Manus on Monday, the immediate reading in the press was that this was about US-China tech decoupling, the limits of “Singapore-washing”, or Mark Zuckerberg’s AI strategy hitting a Beijing wall.

All of that is true. But sitting in Singapore, watching this play out, I think the more interesting question is the one closer to home: what does this episode actually mean for the country trying to position itself as a neutral AI hub, and for the Singapore companies operating under that flag?

What happened, briefly

Manus was founded in China by the team behind Butterfly Effect, made global noise in early 2025 with one of the first credible “general agent” products, and by mid-2025 had relocated its headquarters and most operations to Singapore. In December 2025, Meta announced a roughly US$2 billion acquisition. Meta would absorb the team and technology; Manus would shut its remaining China operations.

In January, Beijing opened a national security and export-control review. The two co-founders were barred from leaving China. On 27 April 2026, China’s National Development and Reform Commission ordered the deal unwound. Meta has signalled it will likely comply. Whether the unwinding can actually be completed is unclear, since the company, the team, and presumably the IP have already been substantially absorbed into Meta.

That is the bare timeline. The interesting parts are the implications.

The “neutral hub” story has always been two stories

Singapore has, for the last few years, been described in international press as a “neutral AI hub” or a “bridge” between the US and China. It is a flattering framing, and it has been useful. But it has been doing two very different jobs at once.

One job is hosting Singapore-grown AI companies, and Singapore-grown AI capability inside SMEs and larger firms, in a jurisdiction that international clients trust. This is the part that benefits us directly. It is the version of the story where Singapore engineering, Singapore data governance, and Singapore corporate structure produce products that are credibly not subject to capture by either Washington or Beijing.

The other job is providing a redomicile address for companies whose technology, talent, and origin remain Chinese, but who want to present a different face to Western customers and investors. This is the “Singapore-washing” version, and it is the one the Manus block has now publicly broken.

These two stories have always coexisted. The trouble is that to outside observers, especially regulators in Washington and Beijing, they look identical at first glance. The Manus episode just made that ambiguity expensive.

What Beijing actually said, and why it matters

The official Chinese position, articulated through the Ministry of Commerce and the NDRC over recent months, is more precise than the headlines suggest. Beijing is not trying to stop Chinese firms from operating internationally. ByteDance, with TikTok, remains the standing example of what is acceptable: international expansion that keeps the core technology, data, and engineering ecosystem rooted in China.

What Beijing is moving against is redomicile as exit. The Manus case establishes the doctrine that technological nationality follows where the technology was built, not where the company is registered. If your founders are Chinese citizens, your model was trained in China, your engineers were trained in China, and your IP originated there, then a Singapore corporate address does not change what you fundamentally are from Beijing’s perspective. It is a position that Lizzi Lee at the Asia Society Policy Institute and Le Xu at NUS Business School have articulated more sharply: corporate identity at face value is no longer accepted by either superpower.

Washington has reached a similar conclusion from the other direction. US regulators are increasingly looking at the full vertical of ownership, supply chain, data flows, and operational control rather than the legal headquarters. The Shein scrutiny is the cleanest example.

Both capitals have, in effect, converged on the same audit standard. Singapore-as-flag is no longer enough on its own.

The awkward truth about “neutrality”

The Singapore position, articulated repeatedly in recent dialogues with industry, is that we do not actually claim neutrality. The argument is that being neutral results in being pulled into a tug of war by major powers. Singapore instead operates on a set of principles, fundamentals, and non-negotiables, communicated candidly to all parties, with positions taken on the basis of national interest. That is a different posture from neutrality. It is closer to what diplomats call principled non-alignment.

The distinction matters for Singapore companies. If you read the international coverage, you would think the country’s pitch is “we are Switzerland for AI”. If you read what the government actually says, the pitch is “we are a reliable jurisdiction with predictable rules and a clear sense of our own interests”. These are not the same product, and they attract different customers.

The first attracts companies looking for a place to hide. The second attracts companies looking for a place to build. The Manus block has just made it costly to confuse the two.

What this means for genuine Singapore companies

First, the “Singapore address” premium is going to compress for ambiguous companies, and possibly expand for unambiguous ones. Genuinely Singaporean AI companies, with Singaporean or naturalised founders, Singapore-trained or Singapore-employed engineers, Singapore-resident data, and operations that are not a thin layer over Chinese infrastructure, are about to look more credible by contrast. Investors and enterprise customers who previously gave a small premium to any Singapore-registered AI firm are now going to ask harder questions. The firms that can answer those questions cleanly will benefit.

Second, SMEs adopting AI need to start reading the geopolitical fine print of their tools. This is the practical part. If your accounting team is using a tool that was Chinese-founded but Singapore-headquartered, your data may sit in a place that is one regulatory action away from sudden change of ownership, sudden withdrawal, or sudden escalation. The Manus episode is not just a story about big M&A. It is a preview of the kind of whiplash that downstream users now have to price in. The two-month rule of thumb I suggest to SMEs I work with: ask where the IP is incorporated, where the founders are passport-holders, where the engineering team physically sits, and where customer data is stored. If those four answers do not point to consistent jurisdictions, you are accepting more political risk than your procurement officer has probably told you about.

Third, the talent corridor is going to get more contested, not less. The MiroMind episode, where Beijing told the company not to send talent abroad after it expanded to Singapore, Japan, and the US, suggests that Chinese AI engineers will increasingly face friction in moving to Singapore even on legitimate paths. This is bad for Singapore’s AI capability building if we relied on that flow. It is, separately, an argument for taking ITE, the polytechnics, the universities, and the SkillsFuture pipeline more seriously as the substrate for AI capability rather than as a fallback. We cannot assume the imported-talent tap stays open at the rate it has been.

Fourth, the brand cost is real. The phrase “Singapore-washing” has now entered the international vocabulary, and unfortunately it does not draw a clear line between cynical redomicile and legitimate relocation. NUS’s Chong Ja Ian has flagged the risk that Singapore is seen as a grey space for technology transfers, which one or both major governments may eventually move to restrict. That is the strategic exposure we should not pretend away. Every Manus-style story costs the legitimate Singapore AI ecosystem a bit of credibility it did not earn the discount on.

What I am watching next

A few things would change my read of this materially. If Beijing accepts a partial unwinding that allows Meta to keep some of the technology and personnel, the deterrent effect of the block weakens, and the redomicile route stays half-open. If Beijing pushes for full reversal and gets it, the door is effectively closed and we should expect a wave of Chinese AI founders making earlier and harder choices, some of which will land in Singapore as genuine relocations rather than transits. Neither of those outcomes is bad for Singapore in the long run, as long as the country is honest about which kind of company it is hosting.

The bigger question is whether Singapore’s official posture stays principle-based or drifts toward a marketed “neutrality” that we cannot actually deliver. The first is durable. The second is rented credibility, and the rent has just gone up.

The bottom line

The Manus block is being read in three capitals as a story about US-China decoupling. From Singapore, I think it is more useful to read it as a stress test of our positioning. The “neutral hub” branding has worked when the stakes were low. The stakes are no longer low. What we have to defend now is not a flag of convenience for transit firms, but the underlying claim that Singapore-grown AI is a substantive category, with substantive standards behind it.

For Singapore SMEs and Singapore-grown AI companies, this is, on balance, an opportunity. The bar for what counts as credibly Singaporean has just risen, and the firms that can clear it have less competition for the trust they earn.

For everyone else, including those of us in policy circles who have been comfortable with the looser version of the story, the Manus episode is the cue to tighten up the language and start telling the truth about what we are actually offering.